What is Control Environment in COSO?

The control environment in Accounting is the set of processes, standards, and structures for the internal control environment, representing the integrity and ethical values of an organization’s operations. It is the foundation component of the internal control framework by the Committee of Sponsoring Organizations of the Treadway Commission (COSO) and provides guidance for setting the widespread tone at the top, embedding a culture of ethical values and integrity throughout the organization.

Institute of Internal Auditors Definition

According to the Institute of Internal Auditors’ definition, the control environment is a foundational pillar of the overall internal control system. It is designed to ensure that:

- An organization achieves critical objectives, including establishing processes to support resource allocation, informed decision-making, and effective performance monitoring.

- Reliable finance statements are produced based on data integrity and controlled transaction processing.

- Internal controls contribute to efficient and effective operations through optimized processes and resource utilization.

- Legal and regulatory compliance is maintained, ensuring adherence to applicable laws, internal policies, and regulations.

- The organization’s critical assets, both tangible and intangible, are protected from theft, misuse, loss, and unauthorized use.

COSO Framework Context

The COSO Framework provides five integrated components or pillars comprised of seventeen principles designed to help achieve three main objectives within an organization.

Three Objectives

- Operating Objectives: Efficiency and effectiveness of the operational and financial performance goals, and securing assets from loss.

- Reporting Objectives: Reliability, accuracy, timeliness, and transparency of internal and external financial and non-financial reporting.

- Compliance Objectives: Adherence to internal policies, state, local, federal, and industry-specific laws and regulations requirements.

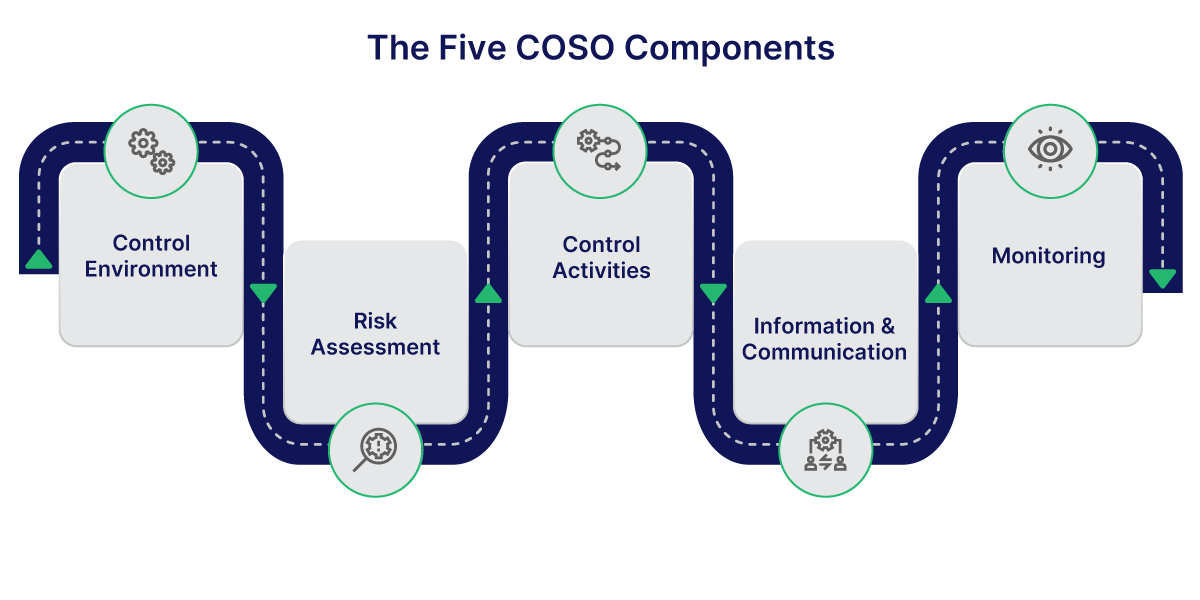

Five Integrated Components

The COSO framework for internal control comprises five integrated components, also referred to as the five pillars, which work together to ensure that overall objectives are achieved.

- Control Environment: Setting up overall culture, discipline, organizational structure, with ethical values, integrity, authority, accountability, and competence from top to bottom across the organization.

- Risk Assessment: Conducting periodic and ongoing identification, analysis, and management of risks to the achievement of objectives, including operational changes and fraud risk.

- Control Activities: Setting up policies and procedures such as addressing risks, approvals, verifications, authorizations, reconciliations, and reviews as manual or automated preventive and detective controls, to help carry out management directives.

- Information and Communication: Setting up comprehensive information systems such as operational, financial, and compliance-related information distribution across the entity with effective communication channels.

- Monitoring Activities: Monitoring internal control processes such as supervisory reviews, performance metrics, and transaction reviews by internal and external audit, including reporting and deficiencies remediation.

Control Environment

As the control environment is the foundational pillar of COSO’s internal control framework guidelines throughout the organization, its effectiveness has a pervasive influence on the other four pillars of the internal control system, including Risk Assessment, Control Activities, Information and Communication, and Monitoring Activities.

A strong control environment fosters a comprehensive culture of integrity and risk awareness, which directly impacts the identification and assessment of risks and reduces the likelihood of fraudulent activities.

A well-designed organizational structure, including segregation of duties, open channels of communication, and a commitment to accountability, ensures that controls are effectively implemented and executed, information flows accurately within the organization, and monitoring activities are performed seriously to identify and address deficiencies promptly.

An effective control environment contributes to a robust internal control system, which ultimately enables an organization to achieve its operational, reporting, and compliance objectives.

Second Pillar: Risk Assessment

Risk assessment involves a set of processes to identify and analyze internal and external threats to an organization’s objectives, determining their impact, prioritizing their nature, and categorizing them so that the most critical ones require a response first. In contrast, less severe risks are managed later, based on their reduced impact.

Risks may be due to technological changes, new regulations, operational breakdowns, economic shifts, or changes in employee composition. Risk assessment is a part of a broader concept, such as Risk Management. These are processes within many organizations’ Enterprise Risk Management (ERM) systems, forming part of their internal control framework, which serves as a foundation for the next component, control activities.

Third Pillar: Control Activities

Control activities refer to the actual actions taken by management to mitigate identified risks through policies and procedures. Actions could include specific steps performed by automated systems or employees, such as approving transactions, reconciling bank accounts, conducting physical inventories, or reviewing performance reports.

Policies dictate what should be done. For example, purchases exceeding $5,000 must be authorized by two managers. This example applies two policies: one is the limit of an amount in currency, and the second is the authorized approval. Procedures outline how policies are implemented, including steps for obtaining approvals and the specific forms used, all of which are documented within a comprehensive routing process.

Control activities can be designed as preventive to stop irregularities from occurring in the first place, or detective, such as finding irregularities after they have occurred, through processes like reconciliations. Control activities should be designed based on the results of the risk assessment process, known as a risk-based approach, rather than a predefined, arbitrary control checklist.

While organizations widely adopt the COSO framework, large and complex organizations may have their own specific needs and context. They can customize different frameworks to achieve their overall objectives with a customized and effective internal control environment.

Fourth Pillar: Information and Communication

Regular communication monitoring helps organizations reinforce the importance of internal controls and an ethical culture. This can be achieved by providing ongoing training programs to educate employees on topics such as data security, compliance requirements, and fraud awareness, as well as customized training tailored to different roles and responsibilities.

Policies should be accessible to all personnel, including governance documents and procedures, to ensure they are easily understood and readily available. Effective communication of critical information should be maintained in both upward and downward directions. This includes utilizing hotline channels for anonymous reporting of control deficiencies, emerging risks, or ethical breaches, as well as providing clear communication from management regarding strategic directions, new policies, changes to existing policies, or performance expectations.

Monitoring Activities

Monitoring activities is the fifth and final pillar of the COSO internal control framework. It is a crucial part to ensure that internal controls are adequate and function as intended. This involves ongoing evaluation of all five pillars, including automated tools such as data analytics, monitoring of applications and their vulnerability mitigation status, automated reconciliations, or review of system-generated reports that provide accurate information about the effectiveness of controls. Internal audits should be conducted for the risk management processes, governance processes, and other processes involved in all five COSO components.

Organizations, especially publicly traded companies, must engage third-party assessments, such as external auditors, consultants, or regulatory bodies, to conduct an independent evaluation of their internal control environment. This evaluation provides insight into and recommendations for improvements. The most important aspect of monitoring activities is identifying deficiencies in the internal control system, reporting them, and addressing these deficiencies promptly by management.

Seventeen Principles

Furthermore, the COSO framework provides 17 fundamental principles that support the five components of internal controls.

- Demonstrating commitment to integrity and ethical values.

- Exercising governance oversight and responsibility.

- Establishing organizational structure, authority, and responsibility.

- Demonstrating commitment to developing competence and retention.

- Enforcing accountability.

- Specifying suitable objectives.

- Risk identification and analysis.

- Fraud risk assessment.

- Significant change in identification and analysis.

- Develop control activities.

- Develop general controls over technology.

- Deploy thorough policies and procedures.

- User-relevant information.

- Internal communication.

- External communication.

- Conducting ongoing assessments.

- Assessment and communication of deficiencies.

Five COSO Principles of the Control Environment

At the heart of the Control Environment pillar of the COSO internal framework are the five principles that provide specific guidelines for establishing a strong ethical and structural foundation for effective internal control within an organization.

Those five principles are as follows:

- Commitment to Integrity and Ethical Values

- Board’s Independence and Internal Control Oversight

- Management Establishes Structures, Reporting Lines, Authorities, and Responsibilities

- Commitment to Attract, Develop, and Retain Competent Individuals

- Accountability for Internal Control Responsibilities

Commitment to Integrity and Ethical Values

The organization should demonstrate a commitment to upholding integrity and ethical values as part of its overall culture. This principle mandates that the effectiveness of overall internal controls starts with leadership, promoting cultural behaviors such as attitudes, actions, honesty, and character. It is about setting the tone at the top and ensuring that these standards and values are communicated and practiced throughout an organization.

Board Independence and Internal Control Oversight

The board of directors should demonstrate independent oversight of internal control, such as the development and performance of the overall internal control environment. It highlights the crucial role of the board in providing unbiased governance by assessing and scrutinizing management actions to ensure the effectiveness of the internal control system, including the design, implementation, and maintenance of internal controls.

Management Establishes Structures, Reporting Lines, Authorities, and Responsibilities

Senior management should be responsible for establishing a clear framework for operations, including creating organizational structures, assigning appropriate authorities to individuals and departments, and defining reporting lines and responsibilities. Management design controls with the board’s oversight to achieve an organization’s strategic goals.

Commitment to Attract, Develop, and Retain Competent Individuals

This principle guides organizations in providing a commitment to attract, develop, and retain competent individuals who are aligned with their objectives. It highlights the importance of human capital in hiring, training, and evaluation, ensuring that the right people with the necessary skills and knowledge are in place to perform their duties responsibly related to internal controls.

Accountability for Internal Control Responsibilities

The last principle in control environment suggests that organizations should hold individuals accountable for their responsibilities regarding internal control to achieve objectives at all levels, ensuring a sense of responsibility and ownership, and taking disciplinary action when there is no compliance with policies.

Approaches

Although these principles offer specific guidance, they are not strict rules. Organizations are expected to adapt these principles as needed, according to their circumstances, complexity, size, and nature, with their own tailored approaches. The goal is to adhere to the principles outlined by COSO for the effectiveness of the Control Environment in establishing and maintaining an integrity and ethical culture across the organization.

Importance of an Effective Control Environment in a Company

The strength of the internal control system determines the likelihood of various outcomes. Strong controls can lead to reliable performance and ongoing success, while weak controls can lead to catastrophic failures and reputational damage.

An example of a weak control system is the scandals involving Enron and WorldCom, where a lack of ethical conduct by top-level management and weaknesses in the control environment in accounting led to significant accounting fraud, misconduct, compliance failures, damage to the companies’ reputations, and resulted in massive fines and penalties.

Another example is the Equifax data breach in 2017 exposing personal information of 150 million people due to a known vulnerability not patched in timely manner and resulted in data breach, this represented different kind of weak control environment that led to non-compliance with laws, regulations and internal control policies and resulted in fines, penalties, legal battles and reputational damage.

That is why a strong internal control environment provides reasonable assurance of compliance with standards, internal policies, and regulations, thereby minimizing legal and regulatory risks.

An effective control environment is not just fulfilling compliance requirements. It is a crucial element for the legitimate success and strength of an organization. It promotes order, discipline, and clarity throughout the organization.

When ethical standards, roles, and responsibilities are in place, operations run more smoothly with fewer errors and redundancies. Management can make more informed decisions based on reliable information, and rework and bottlenecks are reduced through the proper use of resources, leading to increased operational efficiency.

Strong ethical conduct and competence support the delivery of value to stakeholders and the achievement of strategic goals, meeting the core objectives of the COSO framework, including effective operating style, accurate reporting, and ensuring compliance, as well as broader organizational objectives.

Commitment to an effective control environment fosters adherence to industry-related best practices and ongoing improvement, leading to higher performance and governance.

Risk management and protecting company assets from errors, theft, and fraud are valuable benefits of a robust control environment. An ethical culture and awareness of internal controls encourage staff to identify and report significant risks, allowing management to address them promptly.

How to Enhance Control Environment at Department-Level?

The board of directors and senior management establish the overall tone and framework, but the proper control environment management is often reflected at the department level. Policies are implemented within individual departments, and ethical behavior is either routinely evaluated or neglected.

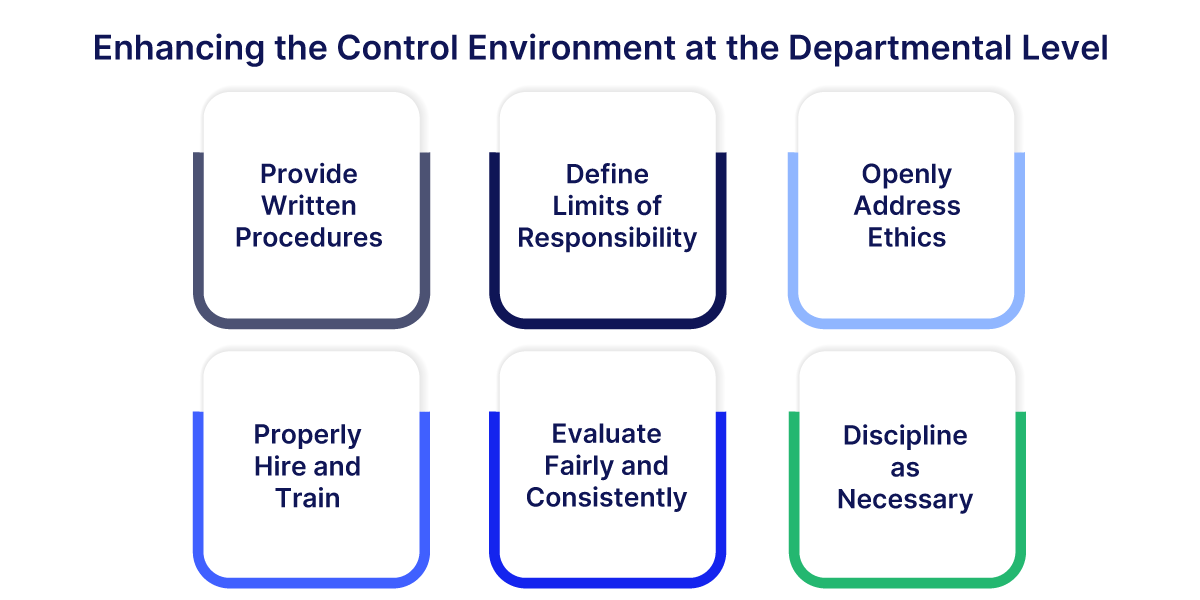

Below are some practical tips for strengthening the control environment at the departmental level.

Provide Written Procedures

Clearly document and provide a general administrative baseline for expected behavior and operations, such as comprehensive employee handbooks, in either hard copy or online form. These written procedures should be provided to employees as a primary reference, containing company-wide policy details, including their rights, benefits, responsibilities, and code of conduct.

Establish specific purchasing manuals that lay out procedures for vendor selection, requisitions, approvals, and payment methods, which are crucial for preventing fraud and securing assets. Tailored departmental manuals provide operational procedures specific to each department, ensuring efficiency and adherence to controls.

Define Limits of Responsibility

Clearly define clarity and limits in roles, including the scope of decision-making power and authority levels for different tasks and transactions, as well as measurable performance standards for each role. Additionally, establish clear reporting lines within the department to higher management. This helps team members to have a clear understanding of their specific responsibilities and how their role contributes to departmental and organizational objectives. This ensures segregation of duties, accountability, prevents unauthorized actions, provides proper oversight, establishes clear communication channels, and outlines escalation procedures.

Openly Address Ethics

Department heads or managers should regularly conduct sessions for open discussions to address ethical understanding and misconduct issues, as well as their implications for the overall control system. This helps in stabilizing ethical considerations in daily work.

Clearly translate department-specific ethical standards that are relevant to the team’s challenges and responsibilities.

Clearly define guidelines for compliance with conflict-of-interest policies to encourage staff to disclose potential conflicts and their proper management.

Properly Hire and Train

Competent staff are the pillar of a controlled environment. Therefore, when hiring individuals for separate roles within departments, ensure that a clear job description is provided outlining internal control responsibilities and expectations.

The hiring process should ensure that competent individuals are hired with the required experience, including background checks, skills, and integrity for the roles.

Offer targeted roles-based training not just for job-specific skills, but also relevant to ethical behavior, awareness of fraud risks, and internal control principles.

Evaluate Fairly and Consistently

Conduct regular performance evaluations for adherence to ethical conduct, policies, and responsibilities to internal controls, recognize satisfactory performance, and reward employees showing strong control awareness and high ethical standards consistently.

Positive reinforcement of periodic performance evaluations encourages desired behavior and career development, while also motivating others.

Discipline as Necessary

Consistently address instances of non-compliance with procedures, policies, and ethical standards promptly and fairly by taking corrective actions such as disciplinary action, documenting them for transparency and audit purposes, and learning from mistakes while supporting standards. This proves that management is serious about accountability and commitment to internal.

Implementation of Internal Control Environment

A practical implementation of Internal Control Environment requires a structured process with careful planning and execution. Steps must be followed to create a strong environment first.

These steps are Vision, Skills, Incentives, Resources, and Plan, often abbreviated as “VISPR”. Skipping the stages can jeopardize and compromise the overall internal control system, which is why order matters. Organizations must establish the Control environment before implementing controls for other components of the COSO framework, such as Risk Assessment, Control Activities, Information and Communication, and Monitoring Activities.

- Vision: Clearly define the required culture, such as ethical standards, values, and expectations, aligning with the objectives of the organization.

- Skills: Ensuring that leadership and employees hired are competent and that they understand the control responsibilities, providing ongoing training on ethics, compliance, and internal control practices.

- Incentives: Conducting performance evaluations, recognition of staff performing well, and awarding them to promote an adherence culture.

- Resources: Creating resource policies and assigning appropriate human resources, technological, and financial resources to support effective internal control.

- Plan: Design a detailed roadmap for internal controls implementation with organizational structure, policies, processes, timelines, duties, and monitoring processes.

Assessing the Internal Control Environment

An Internal Control Environment assessment is a crucial part of ensuring that the control system is working effectively and meeting compliance requirements. Organizations primarily depend on their internal compliance functions and internal audit for assessment. Departments provide independent evaluations of the effectiveness of the control environment, and the compliance functions ensure that the organization is adhering to all applicable laws and regulations.

Many organizations conduct assessments due to regulatory body requirements, such as SOX, SOC, HIPAA, or HITRUST.

- The Sarbanes-Oxley Act (SOX) requires all public trading companies to establish and maintain internal controls over financial reporting, as outlined in sections 302 and 404.

- System and Organization Control (SOC) Reports are used to assess the control environment of the service organizations that provide services to other organizations. Client organizations require them to obtain SOC 1 or SOC 2 reports annually for assurance purposes. SOC1 focuses on internal controls over financial reporting, while SOC2 emphasizes security, availability, integrity, confidentiality, and privacy policies and controls.

- Healthcare provider organizations are subject to the Health Insurance Portability and Accountability Act (HIPAA) and HITRUST certification. They are required to comply with the act to protect the health information (PHI) of patients. To effectively evaluate the control environment, organizations often assign job roles such as Compliance Officer, Regulatory Compliance Specialist, or Compliance Analyst, and hire experts in the relevant fields. If this is not possible, they may employ external independent experts, cybersecurity consultants, or compliance firms.

Improving the Control Environment

Improving the internal control environment is not just a one-time fix but is an iterative journey of assessment and improvement. It is a dynamic and ongoing process that requires attention and adaptation.

Identifying weaknesses in controls and resolving them is a crucial step in improving the internal control environment by conducting regular assessments of specific areas. Then, perform a root cause analysis to identify factors such as a lack of accountability, unclear responsibilities, reluctance to enforce discipline, or insufficient training, and take corrective action to remediate the identified weaknesses.

It is important to note that the improvement level may vary based on the organization’s size, complexity, regulatory requirements, and risk profile.

Small organizations may have less formal but still practical control environments. In contrast, large or complex organizations may require more formal structures, written policies, dedicated compliance functions, and a comprehensive monitoring system to maintain a robust control environment.

Adjust controls as the organization changes. These could include internal changes, such as company growth, the introduction of new product lines, organizational restructuring, or leadership changes. Or external changes, such as advancements in technology, e.g., cloud computing, AI, or emerging cybersecurity threats.

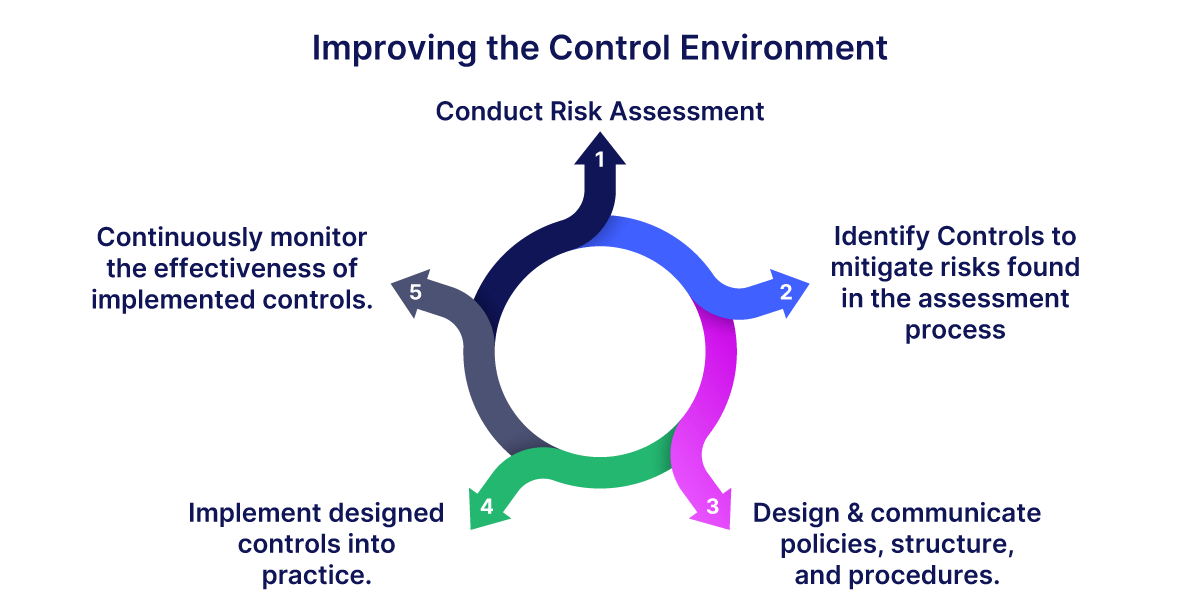

The iterative process for the internal control environment is as follows.

- Conduct Risk Assessment.

- Identify Controls to mitigate risks found in the assessment process.

- Design & communicate policies, structure, and procedures.

- Implement designed controls into practice.

- Continuously monitor the effectiveness of implemented controls.

- Repeat steps 1 to 5 based on the results of monitoring, identified deficiencies in processes, or any environmental changes until the overall internal control environment becomes stronger.

Conclusion

Control Environment is not just a procedural checklist. It serves as the foundation for strong governance, risk management, and compliance in any organization’s internal control system.

An effective control environment enhances operational efficiency, supports the delivery of value, and facilitates the achievement of the organization’s critical objectives by fostering a culture of ethical behavior, integrity, and competence. Business operations are conducted with discipline and structure that reduces errors and increases resource management. Reliable data informs decisions that align with operational, reporting, and compliance objectives, ultimately contributing to the organization’s overall performance and success. A strong control environment requires the ongoing reinforcement of internal control’s role in governance and risk management by setting the tone at the top, accountability for control responsibilities, and proactively finding and addressing weaknesses.

Failing to recognize the importance of a control environment can lead to additional financial and reputational damage, operational failures, and corporate scandals. Therefore, it is the best investment in the long-term prosperity and stability of any organization.